Why There’s No Such Thing as a Quick Estate Plan Review

When someone calls asking for a “quick look” at their estate planning documents, the request sounds simple. Maybe the documents were created online. Maybe they’re a few years old. Maybe there’s been a move to a new state. Most people want a fast yes-or-no answer.

But a proper estate plan review is never quick.

Every will, trust, power of attorney, and beneficiary designation affects your legal, financial, and family outcomes. Reviewing those documents requires legal analysis, asset review, and alignment with current law. Skipping any layer creates risk.

This article explains why a comprehensive estate plan review requires more depth than most people expect, what it actually involves, and why investing in a review now can prevent costly problems later.

The Hidden Complexity of an Estate Plan Review

When you ask an attorney to review your estate plan, you’re really asking several critical questions:

- Are the documents legally valid under current state and federal law?

- Do they still work after a move to a new jurisdiction?

- Do they reflect current tax law?

- Do they accomplish what you believe they do?

- Do all components work together — or conflict?

Each question requires independent legal analysis.

1. Legal Validity Under Current Law

Estate planning laws change. State requirements evolve. Tax exemptions shift. Financial institutions update internal policies.

For example, many banks hesitate to accept a power of attorney that is more than a few years old. If your document is outdated, your loved ones could be denied access to accounts during incapacity.

If you’ve moved to a new state, your documents may still be valid — but not optimal. Differences in probate law, community property rules, or state-specific trust statutes can significantly impact how your plan functions.

A thorough estate planning attorney must analyze how current law applies to your specific situation.

2. Does Your Estate Plan Actually Work?

Many people believe they have a complete plan when they only have a set of documents.

A comprehensive estate plan review evaluates whether your plan addresses:

- Incapacity, not just death

- Minor children and inheritance timing

- Backup beneficiaries if someone predeceases you

- Asset access for surviving family members

- Password and digital asset access

- Insurance sufficiency

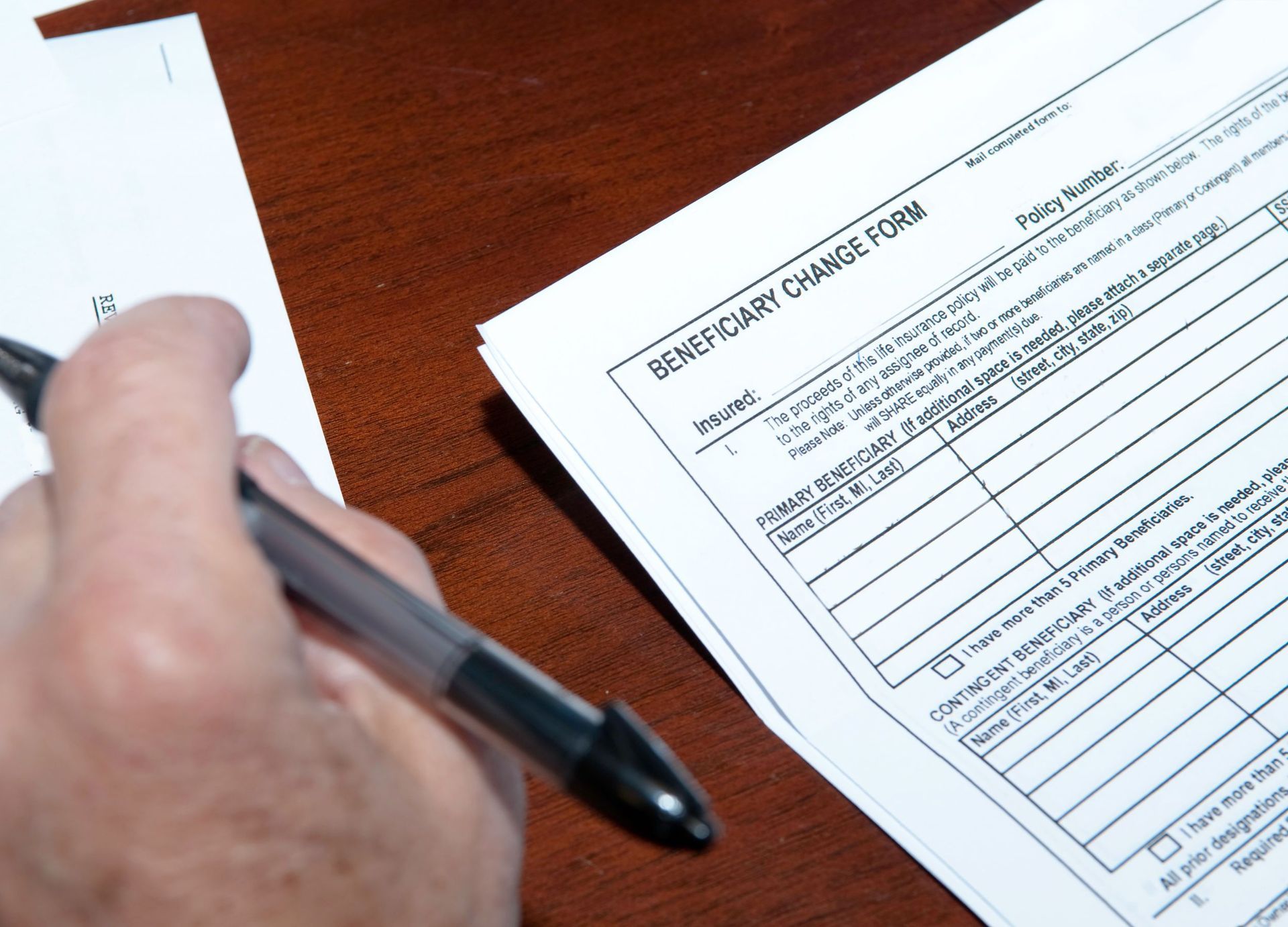

- Updated beneficiary designations

Gaps in these areas often go unnoticed until it’s too late to correct them.

The Most Common Estate Planning Failure: Trust Funding

Here’s what surprises most people:

An unfunded trust does not work.

You can have beautifully drafted documents, but if assets are not properly titled in the trust's name, the trust may be bypassed entirely.

Trust funding requires:

- Reviewing deeds and real estate titles

- Confirming account ownership

- Examining beneficiary designations

- Verifying transfer-on-death (TOD) or payable-on-death (POD) designations

- Coordinating business interests

Even beneficiary designations can override your trust instructions.

Consider this common scenario: your trust directs assets to children in stages, but your life insurance policy names your spouse outright. The payout bypasses the trust. If the spouse later remarries, those funds could pass to unintended beneficiaries.

A proper beneficiary designation review would catch this conflict.

Trust funding is not a five-minute task. It requires methodical analysis of your entire financial picture.

Document Coordination: Avoiding Conflicts and Probate

Estate plan conflicts are more common than most people realize.

A will may say one thing. A trust may say another. Beneficiary designations may contradict both.

When documents conflict, families often end up in probate court for a judge to determine intent. Litigation can cost thousands — sometimes tens of thousands — of dollars, not to mention emotional strain during an already difficult time.

A comprehensive estate plan review ensures all components operate as a cohesive system.

Why Attorneys Cannot Offer “Quick Reviews”

When someone asks for a surface-level review, they are requesting legal advice based on incomplete analysis.

Professional responsibility requires an attorney to either conduct a full review or decline to offer an opinion. There is no safe middle ground.

A proper review includes:

- Detailed document analysis

- Asset inventory

- Funding verification

- Beneficiary alignment review

- Legal research under current law

- Client consultation and recommendations

This process requires time and expertise. It also carries professional liability. That is why comprehensive estate plan reviews typically cost $1,000 or more.

Compared to probate costs, court disputes, or unintended asset distribution, that investment is modest.

What to Expect From a Comprehensive Estate Plan Review

If you pursue a thorough review, expect to:

- Complete a detailed questionnaire

- Provide financial statements and account information

- Share deeds, insurance policies, and business documents

- Discuss family dynamics and goals

- Receive written analysis and recommendations

If updates are needed, those revisions are handled separately.

The goal is not simply to validate documents. It is to ensure your estate planning documents, assets, and intentions align — and will function when your family needs them most.

Peace of Mind Comes From Precision

An estate plan is not a binder on a shelf. It is a coordinated legal system designed to protect your loved ones.

A comprehensive estate plan review protects against:

- Outdated documents

- Invalid powers of attorney

- Unfunded trusts

- Beneficiary conflicts

- Probate exposure

- Family disputes

Quick reviews don’t exist because your family’s future is not simple.

If your documents were created online, drafted years ago, or never reviewed after a move, it may be time for a comprehensive estate planning review.

Schedule a complimentary 15-minute discovery call to ensure your plan works when it matters most.

This material is provided for educational and informational purposes only and does not constitute ERISA, tax, legal, or investment advice. Legal advice specific to your situation must be obtained separately.